'%20fill='%23000000'%3e%3cg%20id='icons'%20transform='translate(56.000000,%20160.000000)'%3e%3cpath%20d='M144,7339%20L140,7339%20L140,7332.001%20C140,7330.081%20139.153,7329.01%20137.634,7329.01%20C135.981,7329.01%20135,7330.126%20135,7332.001%20L135,7339%20L131,7339%20L131,7326%20L135,7326%20L135,7327.462%20C135,7327.462%20136.255,7325.26%20139.083,7325.26%20C141.912,7325.26%20144,7326.986%20144,7330.558%20L144,7339%20L144,7339%20Z%20M126.442,7323.921%20C125.093,7323.921%20124,7322.819%20124,7321.46%20C124,7320.102%20125.093,7319%20126.442,7319%20C127.79,7319%20128.883,7320.102%20128.883,7321.46%20C128.884,7322.819%20127.79,7323.921%20126.442,7323.921%20L126.442,7323.921%20Z%20M124,7339%20L129,7339%20L129,7326%20L124,7326%20L124,7339%20Z'%20id='linkedin-[%23161]'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

'%20fill='%23000000'%3e%3cg%20id='icons'%20transform='translate(56.000000,%20160.000000)'%3e%3cpath%20d='M335.821282,7259%20L335.821282,7250%20L338.553693,7250%20L339,7246%20L335.821282,7246%20L335.821282,7244.052%20C335.821282,7243.022%20335.847593,7242%20337.286884,7242%20L338.744689,7242%20L338.744689,7239.14%20C338.744689,7239.097%20337.492497,7239%20336.225687,7239%20C333.580004,7239%20331.923407,7240.657%20331.923407,7243.7%20L331.923407,7246%20L329,7246%20L329,7250%20L331.923407,7250%20L331.923407,7259%20L335.821282,7259%20Z'%20id='facebook-[%23176]'%3e%3c/path%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e)

In 2024, Australian insurer NIB paid out more than AUD $3 million for a claim. The patient needed treatment in ICU and eventual repatriation from the USA. Could you afford to pay that? If not, you’ll need to look at international health insurance.

If you’re living in a country without access to a universal healthcare system, even small medical expenses will start to add up. For most people, they wouldn’t be able to afford that headline figure and could find themselves in debt or stranded overseas without the right insurance.

- What is international health insurance?

- Why expats need international health insurance

- Types of international health insurance coverage

- Basic vs. premium coverage levels

- Essential benefits to look for

- Factors that can affect your premium

- International health insurance providers: our recommendations

- How to choose the right international health insurance

- Eligibility criteria

- Getting started: your next steps

- International health insurance: readers’ questions

What is international health insurance?

International health insurance covers your health needs when you’re living overseas. It’s designed for people who are living, working or travelling away from their home country. It provides a financial safety net if you ever require treatment.

Whereas you might rely on the public health system when you’re at home, international health insurance covers you while you’re away. It can cover you for emergency treatment and routine care, depending on your policy.

Most policies cover you for the long term, so over a year. For shorter amounts of time, travel insurance might be more appropriate.

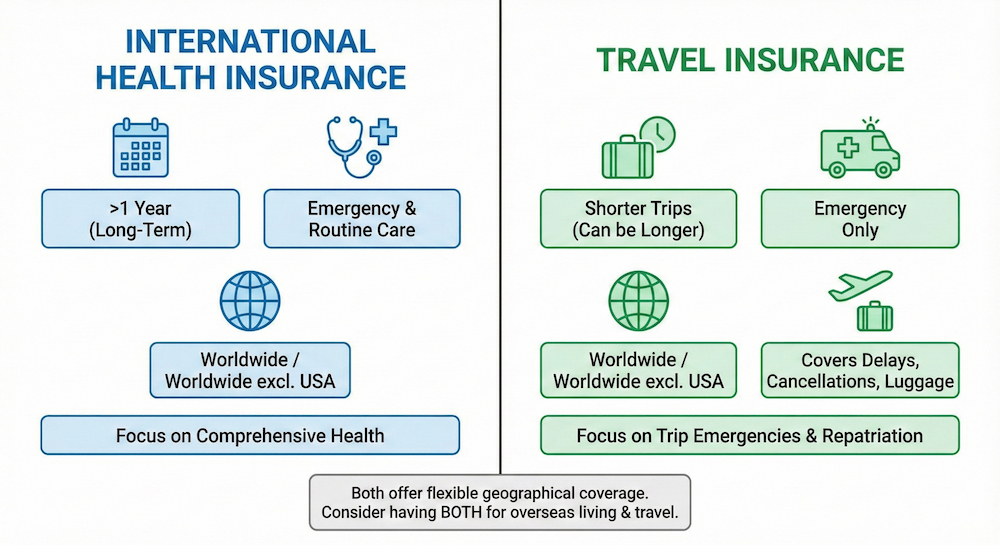

International vs. travel insurance: key differences

International health insurance generally covers you for over a year, while travel insurance is usually for shorter trips. That said, you can get longer-term travel insurance.

One key difference is international health insurance covers you for emergency treatment and routine care. Travel insurance only covers you in an emergency. If you need more treatment your policy should cover the costs of getting you home.

For both types of insurance, where you’re covered depends on the policy you’ve purchased. You should always make sure you’ve got the correct cover. Common options include worldwide or worldwide excluding the USA. The latter is usually cheaper, given the high cost of healthcare in the USA.

If you’re travelling exclusively in one country or continent, you might be able to save money and buy a policy just for there.

Travel insurance can also cover for delays, cancellations and luggage, so if you’re living overseas and travelling, you might opt to have international health insurance and travel insurance.

Why expats need international health insurance

Visa and legal requirements

For some countries, health insurance is a requirement when you’re applying for a visa. This is so you’re not a burden on the health system there and also so you can afford to be evacuated if it’s medically necessary. You won’t become bankrupt if you need treatment.

In other cases, you might be able to get travel insurance for when you arrive in a country, then have access to its health system. This could be through an employer or reciprocal healthcare agreement.

Either way, it’s important to know the requirements before you apply and make sure you’re going to be covered.

- Australia: Nearly all work and study visas in Australia require you to have health insurance. You’re likely to be asked for proof of cover when you apply. It’s possible to buy a policy from a global provider or purchase a purpose-built plan from an Australian employer.

- Germany: D visa (stays over 90 days). In Germany, ou’re required to have health insurance that covers the minimum level of the statutory health insurance system. Travel insurance is not an option.

- Dubai: If you apply for a Digital Work Visa you can live and work in Dubai for 12 months. To qualify you need to have adequate health insurance for the entirety of your stay.

Healthcare gaps when living abroad

If you have private healthcare in your home country, the chances are that it’s based on residence. So if you leave your country and are no longer a resident, your coverage is likely to end.

When you move overseas, you’re may have limited or no access to the local healthcare system. The best way to cover yourself is by having some form of health insurance.

You also have to factor in that healthcare varies in quality depending on where you are. Having private health insurance means you’ll be able to get a greater level of cover, should you need it.

Financial protection benefits

International health insurance can stop you going into debt to cover your health needs. Healthcare can be exorbitant in certain countries and you might not even be treated if you can’t prove your cover, even in an emergency.

The cost of healthcare can vary significantly among destinations that are popular with expats.

Here is an example of estimated costs in three countries:

- In the UAE, a routine doctor’s visit could cost between AED 250 and AED (around £50–£60.

- In Thailand, the same visit could cost from as little as ฿100 to ฿300 (around £2–£7).

- In Spain, it could cost you between €45 and €70 (around £40–£60).

Emergency evacuation costs can end up costing hundreds of thousands of pounds. For most people that’s not affordable without health insurance.In 2024, the BBC reported about a young woman who had a £100,000 bill after a rejected insurance claim because the information given wasn’t correct when the policy was taken out. This shows not just the importance of health insurance but also why you need to make sure your details are correct.

Types of international health insurance coverage

There’s a wide range when it comes to choosing the type of coverage you need for your international health insurance.

You’ll need to consider what level of cover you need. If you’re going to be living in a cheaper country, where healthcare costs are lower, you might not need full coverage. Routine care might be cheap enough as it is and you could then just have health insurance to cover you in an emergency.

On the flipside, if you’re going somewhere with high healthcare costs, a comprehensive plan is likely to be more suitable. You don’t want to pay through the nose for simple things like visiting a doctor or prescription medication.

Another thing to consider is where you need coverage.

If you’re only staying in one country or region, you might be able to save money by getting a policy just for there. If you’re travelling more, then you might need worldwide coverage.

The USA has among the highest costs of healthcare in the world, so having a policy that covers the USA will cost you more. Think about if you’ll be going there and if it’s worth paying extra to be covered.

Basic vs. premium coverage levels

Every policy and insurer is different. To give you a sense, this is what Allianz offers:

| Basic | Mid-range | Premium |

|---|---|---|

| Semi-private room Diagnostic tests Surgeries Oncology Rehabilitation treatment Nursing at home Emergency out-patient treatment | Private room Diagnostic tests Surgeries Oncology Rehabilitation treatment Nursing at home Emergency out-patient dental treatment Option to add maternity | Private room Diagnostic tests Surgeries Oncology Rehabilitation treatment Nursing at home Emergency out-patient dental treatment Option to add maternity Laser eye treatment Preventative Surgery Accidental death benefit |

| Max. Plan Limit: £1,575,000 €1,851,850 USD $2,500,000 | Max. Plan Limit: £2,460,000 €2,963,000 USD $4,000,000 | Max. Plan Limit: £3,100,000 €3,703,705 USD $5,000,000 |

*As at 19 November 2025

Most providers should also allow you to choose your deductible (excess).

A plan with a higher deductible usually has lower premiums. If you have a lower or no deductible, your premiums are likely to be higher.

This is a personal preference and you should also factor the cost of healthcare in the places you plan to live or travel.

Essential benefits to look for

These are the kinds of coverage that most basic plans will have:

- Inpatient hospitalisation

- Outpatient care

- Emergency services

- Specialist consultations

- Prescription medications

In addition, premium plans might have the following available:

- Maternity care

- Dental and vision

- Mental health services

- Preventive care

- Telemedicine

Are emergency services covered?

Yes, emergency services are covered. This is arguably the most important factor in having international health insurance.

Let’s say you’re overseas and you injure your leg, you might need an ambulance. The ambulance would take you to the nearest hospital, where you might require surgery after the doctors discover you’ve broken your leg. This would be covered by your health insurance and in many cases could be covered by direct billing. So you won’t have to worry about any of the financial elements and can focus on healing.

Are emergency services covered?

Yes, emergency services are often covered. This is arguably the most important factor in having international health insurance.

Let’s say you’re overseas and you injure your leg, you might need an ambulance. The ambulance would take you to the nearest hospital, where you might require surgery after the doctors discover you’ve broken your leg. This would be covered by your health insurance and in many cases could be covered by direct billing. So you won’t have to worry about any of the financial elements and can focus on healing.

Factors that can affect your premium

- Age and health status. As a general rule, the younger you are and the healthier you are, the cheaper your policy will cost.

- Coverage area selection. Some areas will cost more to insure. The biggest example would be for policies that include cover for the USA.

- Deductible amount. If you have a lower deductible, your premium is likely to be higher.

- Benefit levels chosen. The more conditions you have cover for, the more you’re going to pay.

- Pre-existing conditions. These can push up the cost of your policy, but it’s important to declare them so you’re properly covered.

- Country of residence. Where you’re from can impact what your policy might cost.

International health insurance providers: our recommendations

Cigna Global Health Insurance

Cigna has a global network of 1.5 million hospitals and healthcare providers in over 200 markets and territories. It also offers 24/7 multilingual customer service.

It has four different plan options. Its policies are customisable, so you can choose a core policy and add any extras you think you’ll need.

You can choose the deductible you want, with options ranging from USD $0 to USD $10,000.

You also choose your cost share percentage, which is the percentage of each claim not covered by your plan. It ranges from 0% to 30%.

And finally you get to choose your out-of-pocket maximum amount, which can be USD $2,000 or $5,000.

Allianz Care International Health Insurance

Allianz Care has over 2 million providers in its global network, available in over 200 territories.

It has three plan tiers for you to choose from. You can enhance your cover with add-ons if you need.

Once you choose a plan tier and add-ons, you’ll have the option to pay in full or in regular instalments. If you don’t pay in full then a surcharge will be added to each payment.

April International Health Insurance

April has been operating for over 40 years. It has a network of over 2 million providers in 180+ countries.

It has the choice of four tiers. You can customise your plan to suit your needs. If you have a family plan, you can choose different levels of cover for each person.

In terms of pricing, April lets you choose your deductible and whether you want to pay monthly, annually or quarterly, in some cases.

How to choose the right international health insurance

There’s no one-size-fits-all approach when it comes to choosing a policy. You’ll need to decide what you need before you purchase. This can include:

- Current health status. Make sure you choose a plan that covers your current needs and any pre-existing conditions you might have. You should also consider what might come up in the future and plan for that.

- Planned countries of residence. Some plans let you choose a specific country or region.

- Duration of coverage needed. Always ensure you’re covered for the duration of your stay. If you’re unsure, then you might think about opting for a plan that makes renewal easy.

- Budget considerations. Getting a range of quotes from different providers can help you find a quote in your price range.

- Family coverage requirements. Are you going with a partner or children? Do you plan to have children while you’re living overseas?

Questions to ask providers

You should ask providers if they cover any pre-existing conditions and if there are any waiting periods around that. Not being upfront could void your policy or leave you out of pocket in future.

Most providers say how quickly they plan to process claims. You should ask about their process and how easy it is to claim. For many policies this can be done on an app or website, but more complex claims could involve a longer process.

Does the insurer have a large network of healthcare providers that’s easy to access? It makes sense to make sure where you’re going is well covered so you’re not travelling far for care.

Do you feel comfortable with the policy’s emergency procedures? There can be some variation between providers, so you want to know what you can expect.

Eligibility criteria

- Most international health insurance policies have residency requirements. They typically start with you being abroad for at least three months. If you’re going for less than that then travel insurance might be more appropriate. But it depends on what you need cover for.

- Each insurer will have a different set of age requirements. In general you can get cover once you’re 18. As you get older, there might be more exclusions for certain conditions.

- Check the policy you’re buying is available for your nationality. An example of this is that American citizens might only be able to buy a policy if they’re planning to be overseas for a certain amount of time.

Required documentation

- Passport/ID verification

- Proof of residence abroad

- Medical history questionnaire

- Previous insurance certificates

Getting started: your next steps

When you start looking for international health insurance, these are the steps you should take:

- Request quotes from multiple providers. This will ensure you can choose the price that gives you the most value.

- Compare coverage options. Best value doesn’t always mean the best price. If a policy covers more it’s likely to cost more, but that might suit your needs better.

- Consult with insurance specialists. You can talk to experts to get a better idea of the best policy for you.

- Apply 30-45 days before departure. You want to make sure you’re covered before you leave. Some visas will require you to purchase coverage when you apply, so make sure you do your research in advance. If you do need to purchase when applying for a visa, you can choose your policy start date to align with when you leave your home country.

International health insurance: readers’ questions

How does worldwide coverage work?

Worldwide coverage typically covers the whole world or can be bought excluding the USA. Simply put, if you have worldwide coverage then you’ll be covered everywhere you go. But you should still check the terms and conditions of your policy to make sure you have the right level of cover.

Can I add family members?

Yes, you can add family members. Plans can be for individuals, couples or families. There are sometimes discounts for family members.

How are premiums calculated?

Health insurance premiums are calculated based on a number of factors. These include age, where you’re going, any pre-existing conditions, the level of cover you want and the deductible (excess).

How long do claims take?

Some insurers offer direct billing, meaning payment is managed between the healthcare provider and the insurer. As an example, Allianz says it can pay some claims within 48 hours. Cigna and April say they try to pay within five days.

What if I can’t find a network provider?

If you can’t find a network provider, you should contact the insurer. Most have 24/7 support and will be able to help you with your options. In some cases you can get treatment out of network and submit a claim. You might end up having to pay a higher deductible (excess). It all depends on the terms and conditions of your policy, so speaking to your insurer is the best place to start.

How do I change my coverage?

The best option is to speak to your insurer to find out if you can change your plan. Often you can downgrade your plan, but you might not get a refund. If you want to upgrade your plan, you might need to do a medical review. It can look suspicious if you suddenly want extra cover.